The Power of Partial Budgeting in Dairy Decision Making

The Power of Partial Budgeting in Dairy Decision Making

When you have a decision to make, how do you make that decision? For most of us, our decisions are based largely on intuition, gut feel, or past experiences. Sometimes, this decision making practice work, and sometimes it doesn't. In any competitive business, making the right or best decision is critical to out-competing other businesses. Certainly, in today's dairy economy, any competitive edge may be the difference between surviving or leaving the dairy business. Unfortunately, too many dairy decisions are made without a true economic evaluation of the implications of the decision. Fortunately, there are numerous tools available to help dairy producers make more informed decisions. Progressive dairy producers have already begun to adopt some of these tools and others should follow. While more sophisticated decision making tools and techniques are on the horizon, let's examine the power of a very simple technique called partial budgeting.

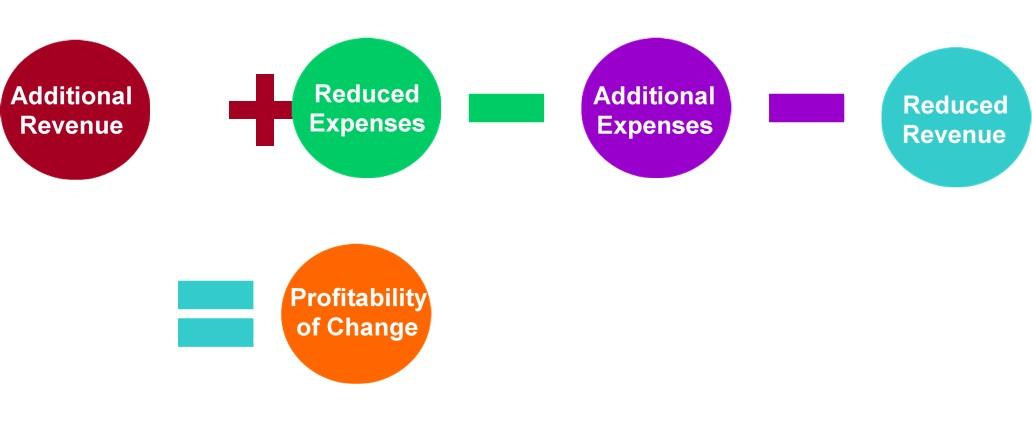

Whether you realize it or not, you are probably very accustomed to the practice of partial budgeting, at least in an informal manner. A partial budget is used to calculate the expected costs and benefits of alternatives encountered by a dairy business. What makes the partial budget so appealing is that this type of analysis focuses on only revenue and expenses affected by a proposed change or intervention. Typically, these changes are divided into four categories: (1) additional revenue, (2) reduced expenses, (3) reduced revenue, and (4) additional expenses. This type of analysis focuses on identifying the expected net change in revenue and expenses resulting from proposed changes rather than determining the entire profit and loss of an operation. This method is less time-consuming than complete budgeting because the focus is on a few variables rather than the complete system. One must be cautious in interpreting the results of a partial budget because they do not properly account for all possible benefits and costs, the timing of revenue and expenses, and uncertainty associated with the decision. Examples of dairy decisions where a partial budget approach is appropriate include: use of a feed additive, 2X versus 3X milking, installing cooling systems in a barn, hiring custom work, using sexed semen, and leasing versus buying equipment. On the other hand, a partial budget might not be appropriate for major capital investments or

decisions that would alter the structure of the business.

To create a partial budget, one needs to have some idea of the potential impacts of the proposed change. Often, insufficient data exists and we are forced to make our best educated guess. Ideally, the information used in a partial budget should be based on peer-reviewed research demonstrating impact across multiple farms. When this information is not available, we will need to use the best information at hand, either from industry professionals or other farmers with experience implementing the proposed change. Whatever numbers we ultimately use should be based on sound assumptions. Conservative estimates will generally provide more realistic, less risky results than overly optimistic projections.

The general equation for a partial budget analysis is provided in Figure 1. Essentially, we are trying to estimate any changes in revenue or expenses associated with the proposed change. Estimates for each of four categories ((1) additional revenue, (2) reduced expenses, (3) reduced revenue, and (4) additional expenses) should be obtained prior to running calculations. Remember that we are only looking at impacts resulting from the proposed change. The net profitability of the change is calculated by subtracting additional expenses and reduced revenue from additional revenue and reduced expenses. A positive net profitability would generally indicate a good decision for the business while a negative net profitability would indicate an undesirable decision. Of course, higher profitability estimates would provide us more confidence that the decision is the right thing to do.

The most simple partial budgets can be performed with a pencil, paper, and a calculator. Just writing the numbers down and working through the calculations can be a valuable exercise. Often, though, the calculations can quickly become overwhelming; thus, spreadsheets are commonly employed in partial budget analyses. Not only do spreadsheets make the calculations easier but they also open the doors for more detailed examination of the decision. With a spreadsheet, we can easily perform sensitivity or "what if" analyses. For example, we can determine how the decision changes based on number of cows in the herd, pounds of milk gained by implementing a practice, or the cost of whatever practice or technology is being considered. It can be useful to run three analyses under (1) anticipated, (2) worst-case, and (3) best-case scenarios. This type of sensitivity analysis can provide considerable insight into the amount of risk involved in the decision and can help scrutinize assumptions used. If you aren't comfortable or don't have the time to build a spreadsheet, there are dozens of already developed partial budget spreadsheets available online focused on dairy-specific decisions. In addition to saving time working through calculations, these spreadsheets often have assumptions already built-in. Examples can be found from the Wisconsin

Center for Dairy Profitability (http://cdp.wisc.edu/), the University of Florida (http://dairy.ifas.ufl.edu/tools/index.shtml), the Pennsylvania State Dairy Alliance (http://dairyalliance.psu.edu/im/organization) and the University of Wisconsin Extension Forage Resources

(http://www.uwex.edu/ces/crops/uwforage/dec_soft.htm). A simple Google search can lead you to the appropriate spreadsheet for your decision. If you are unable to find an existing spreadsheet, contact your county agriculture agent, trusted industry advisor, or state dairy extension specialist to help you develop a new one.

Ultimately, a partial budget analysis does not tell decision makers what to do, but it provides them with a more detailed perspective on the economic implications of the decision. The next time you have a decision to make, consider using a partial budget approach to assist in the decision making process!

Figure 1. Simple equation for a partial budget.

Author: Jeffrey Bewley